Learn more

Getting Started Community Digital Products Growing Your Business Crypto Payments Making MoneyFree tools

Mockup GeneratorDocumentation coming soon

Follow us

Learn more

Getting Started Community Digital Products Growing Your Business Crypto Payments Making MoneyFree tools

Mockup GeneratorDocumentation coming soon

Follow us

If you are searching for a Whop alternative for digital products, you have probably already hit the wall that makes sellers start looking. Chargebacks that eat into revenue you already earned. Marketplace commissions that take 30% of sales Whop’s Discover feature drives to your listing. Reserve holds that lock up your cash based on a dispute risk score you cannot fully control.

Whop works. But it works within the same card-based payment infrastructure that gives buyers the power to reverse transactions after consuming your product. This guide compares Whop’s model against a crypto-native approach where chargebacks do not exist by design, payouts hit your wallet the moment a sale confirms, and no platform holds custody of your funds.

In This Article

Whop built its reputation as an all-in-one platform for creators selling digital products, memberships, and community access. It handles checkout, delivery, and even offers a marketplace called Discover where buyers browse and purchase products directly. For early-stage sellers, that bundled approach saves time.

The friction shows up once revenue grows. Whop’s Discover marketplace charges a 30% commission on any sale that originates from their marketplace or through an affiliate referral. That is not a processing fee. That is nearly a third of your revenue on every marketplace-driven transaction.

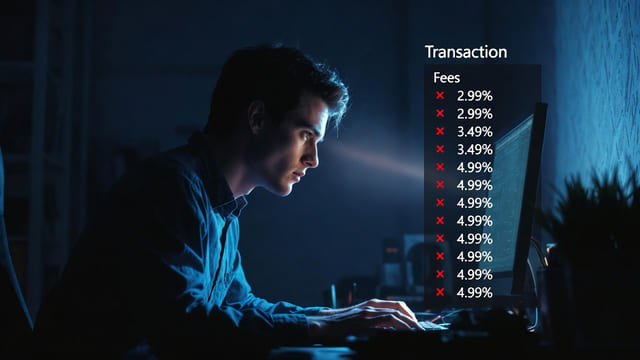

Even on sales you drive yourself, the fee layers stack. The base platform fee is 3% on sales involving automations like Discord or Telegram role assignment. On top of that, card processing runs 2.7% plus $0.30 per domestic transaction. International cards add another 1.5%. Currency conversion adds another 1%. A $50 product sold to an international buyer through Whop’s marketplace could lose close to 35% of the sale price before a single cent reaches your account.

The cost of selling on any platform is not just the headline fee. It is the total percentage of revenue that actually reaches your wallet after every layer is applied.

Beyond fees, there is the structural issue that every card-based platform shares: chargebacks. Whop processes payments through traditional card networks. That means buyers can dispute charges through their bank after receiving your product. Whop charges a flat fee per chargeback or dispute, and if your dispute rate climbs, the platform applies reserve holds to your future payouts. Your money sits in Whop’s system until the risk score improves.

For sellers who want a Whop alternative for digital products that eliminates these problems at the infrastructure level, the answer is not another card-based platform with slightly different fees. It is a fundamentally different payment model.

Whop advertises itself as free to start, and that is true. There are no monthly subscription costs. But the transaction-based fee model means costs scale directly with revenue and can compound in ways that are not obvious from the pricing page.

Here is what a Whop seller actually pays per transaction:

Whop also implements reserve holds based on your dispute risk score. New sellers and sellers with elevated chargeback rates may have a percentage of each sale held back for a set period. This is not uncommon for card-based platforms, but it directly contradicts the idea of instant access to your earnings.

None of this makes Whop a bad platform. These are the structural realities of any business built on traditional card payment rails. Visa and Mastercard set the rules. Processors enforce them. Platforms pass the cost to sellers. If you sell digital products at volume, especially to an international audience, these costs compound fast.

A seller doing $5,000 per month on Whop through a mix of marketplace and self-driven sales could pay between $300 and $800 in combined fees, reserves excluded.

The question is not whether Whop’s fees are fair for what they offer. The question is whether the underlying payment infrastructure is the right fit for your business model. For many digital sellers, the answer increasingly points toward stablecoin payment infrastructure that removes most of these cost layers entirely.

Fee comparisons between platforms miss the single largest hidden cost for digital product sellers: chargebacks. A chargeback is not a refund. It is a forced reversal initiated by the buyer’s bank, and the seller has almost no power in the process.

Digital products are the most vulnerable category because there is no physical item to return. A buyer purchases your prompt library, downloads every file, and files a dispute three weeks later claiming the charge was unauthorized. The bank sides with the cardholder by default. You lose the revenue, pay the dispute fee, and the buyer keeps your product.

Whop has a Resolution Center where sellers can attempt to resolve disputes before they escalate to the card network. That helps in some cases. But once a buyer goes directly to their bank, the Resolution Center cannot override the card network’s decision. The chargeback mechanism is built into the payment infrastructure itself, and no platform policy can fully eliminate it as long as card payments are involved.

The compounding effect is what causes the most damage. Card brands monitor your chargeback ratio as a percentage of total transactions. Cross 1% and your processing costs increase, monitoring programs activate, and in extreme cases your merchant account can be shut down entirely. For a seller doing 200 transactions per month, just two successful chargebacks put you at the threshold.

Chargebacks do not scale linearly with revenue. They scale with visibility. The more successful your product becomes, the more exposure you carry.

This is not a Whop-specific problem. It applies to every platform built on Visa, Mastercard, and traditional card processing. Blockchain-based payment infrastructure eliminates this risk at the architectural level because there is no card network to initiate a reversal through.

The reason crypto-native platforms can guarantee zero chargebacks is not a policy decision. It is how the technology works.

When a buyer pays in USDC on Solana or Base, the transaction confirms on-chain in seconds. Once confirmed, it is cryptographically final. There is no card network sitting between buyer and seller with the authority to reverse the transaction. There is no bank that can pull funds back at the buyer’s request. The payment is settled, permanent, and in the seller’s wallet.

This is fundamentally different from card-based platforms where every transaction carries an implicit 120-day reversal window. On a blockchain, that window does not exist. A completed sale is a completed sale. Period.

USDC is a stablecoin pegged 1:1 to the US dollar, issued by Circle. Receiving payment in USDC means you are not exposed to crypto price volatility. You get dollar-denominated revenue that settles instantly. You can hold it in USDC, withdraw to any wallet you own, or convert to fiat through exchanges like Coinbase or Kraken within minutes.

For sellers evaluating a Whop alternative for digital products, this is the core differentiator. It is not about slightly lower fees or a different dashboard layout. It is about whether completed sales stay completed. On card-based platforms, they might not. On crypto-native platforms, they always do.

Read more about how USDC works and why sellers use it for a full breakdown of the stablecoin mechanics.

Summon+ is a crypto-native digital marketplace built on Solana and Base. It is designed specifically for digital product sellers who want instant payouts, zero chargebacks, and full control over their revenue from the moment a sale confirms.

The structural differences between Summon+ and Whop:

Summon+ supports the same product types Whop sellers are familiar with: digital downloads, gated Discord access, recurring subscriptions, tiered membership plans, and one-time payments. The difference is in how payments settle and who controls the funds after a sale.

For sellers coming from Whop who run paid Discord communities, the Discord integration on Summon+ handles automated role assignment on purchase. Connect your server in the Integrations tab, map each product to a role, and access is granted automatically when a buyer completes checkout. No manual approvals, no bots to configure separately.

A direct comparison helps clarify where each platform fits. Both serve digital product sellers. The difference is in the payment infrastructure and what that means for your revenue.

Payment model: Whop processes card payments through traditional processors. Summon+ settles all payments in USDC or USDT on Solana and Base. When card payments launch on Summon+, buyers will purchase USDC through the payment rails. The seller always receives stablecoins.

Chargebacks: Whop is exposed to chargebacks on every card transaction. Sellers may incur dispute fees and reserve holds. Summon+ has zero chargebacks by design because blockchain transactions are irreversible once confirmed.

Payout speed: Whop offers daily payouts but may apply reserves that delay access to funds. Summon+ payouts are instant with no approval queue and no reserve mechanism. Funds go directly to your wallet the moment you withdraw.

Fund custody: Whop holds seller funds on the platform until payout. Summon+ does not custody funds. Revenue settles directly to the seller.

Marketplace commission: Whop charges 30% on sales from Discover or affiliate referrals. Summon+ does not apply a 30% marketplace commission.

Discord integration: Both platforms support gated Discord access with automated role assignment. Whop integrates through its own automation layer. Summon+ connects through the Integrations tab with direct server mapping.

Product types: Both support digital downloads, memberships, subscriptions, and community access. Summon+ additionally supports tiered membership plans with monthly, quarterly, and yearly billing cycles in USDC.

The comparison is not about which platform has more features. It is about which payment infrastructure protects your revenue and gives you immediate access to what you earn.

Not every seller needs to move. The right Whop alternative for digital products depends on your selling model, your audience, and how much chargeback exposure your product category carries.

Sellers who benefit most from switching to a crypto-native platform:

Sellers who may want to stay on Whop:

The decision comes down to one question: is your current platform’s payment infrastructure helping or hurting your revenue at the margin you are operating at? If chargebacks, reserves, and stacked fees are eating into what you earn, the infrastructure is the problem. Not the features.

The best Whop alternative for digital products is not the one with the lowest headline fee. It is the one where completed sales stay completed, payouts arrive instantly, and no platform holds custody of your revenue.

Summon+ was built on that principle. Instant USDC payouts, zero chargebacks by design, automated Discord integration, and a built-in affiliate system that pays commissions in stablecoins. If Whop’s fee layers and chargeback exposure are limiting your growth, Summon+ is worth comparing directly. For a broader look at how crypto-native platforms stack up against traditional options, explore the no chargeback selling guide.

Whop has no monthly subscription fee, but it charges a 3% platform fee on sales with automations, 2.7% + $0.30 per card transaction, additional fees for international cards and currency conversion, and a 30% commission on sales originating from its Discover marketplace. Chargeback disputes also carry a flat fee per incident.

Yes. Running both platforms simultaneously is a common migration strategy. List your products on both, share Summon+ checkout links with your crypto-native audience, and keep Whop active for buyers who prefer card payments. Once you confirm which platform drives better net revenue, you can consolidate.

Buyers pay in USDC or USDT, which requires a wallet. However, Summon+ is adding card payment support (Visa, Mastercard, Apple Pay) where buyers purchase USDC through the payment rails automatically. The seller always receives stablecoins regardless of how the buyer pays.

Since blockchain transactions are irreversible, there is no forced chargeback mechanism. Refund policies are set by the seller. You decide whether and when to issue a refund. This gives sellers full control over refund decisions rather than leaving them to a bank or card network.

Yes. Summon+ offers automated Discord role assignment. Sellers connect their server in the Integrations tab, map each product to a specific role, and buyers receive their role automatically the moment checkout completes. No manual approvals or third-party bots required.

Join Summon+ Marketplace and start selling your digital products with instant crypto payouts. Set up your store in under 2 minutes.